Should I use Buy Now Pay Later or a credit card?

If you’ve ever paused at checkout asking yourself this question—you’re not alone.

With BNPL services like Tabby and Tamara becoming increasingly popular in the UAE, and credit cards still dominating everyday spending, choosing between the two can feel confusing.

At first glance, both seem similar:

You don’t pay everything upfront

You can spread payments over time

But in reality, they work very differently—especially when it comes to costs, risks, accessibility, and long-term financial impact.

What This Guide Will Help You Understand

- In this UAE-focused guide, we’ll break down:

- The real difference between BNPL and credit cards

- Which option is cheaper (and when)

- How each one impacts your credit score

- When you should use BNPL vs a credit card in real life

Let’s break it down 👇

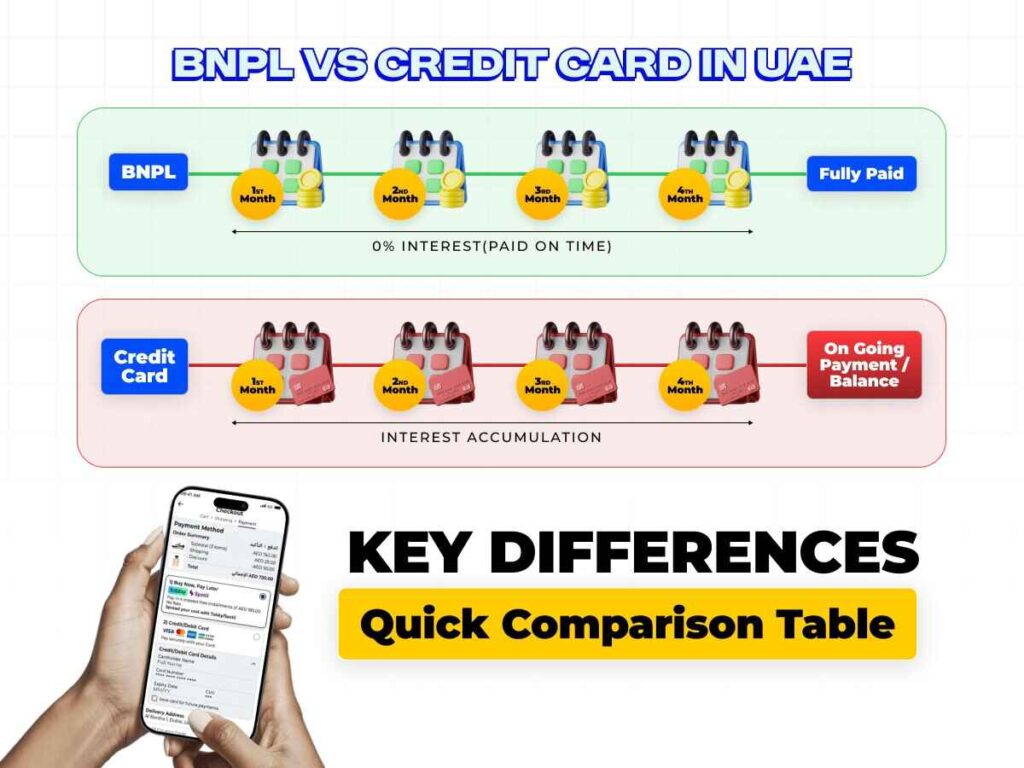

BNPL vs Credit Card in UAE – Key Differences (Quick Comparison Table)

If you’re looking for a quick answer, this table gives you a high-level snapshot of how BNPL and credit cards compare.

| Factor | BNPL | Credit Cards |

| Repayment Type | Fixed instalments (clear end date) | Revolving credit (ongoing balance) |

| Interest / Fees | 0% if paid on time; late fees (capped) | 0% if paid in full; otherwise ~2–4% monthly interest (compounding) |

| Accessibility | Easy approval, minimal requirements | Requires salary, credit score, bank approval |

| Credit Score Impact | Limited positive impact; missed payments can hurt | Strong impact; builds credit if used responsibly |

| Flexibility | Limited to partner merchants | Widely accepted globally |

| Cost Risk | Predictable and capped | Can grow over time if unpaid |

| Best Use Case | Short-term, planned purchases | Everyday spending, travel, credit building |

👉 Use this table as a quick reference, then explore the sections below for detailed insights.

Smart Move : Before choosing BNPL or a credit card, you can save more upfront by checking QYUBIC—where you’ll find exclusive promo codes across top brands, with discounts of up to 70%.

How Credit Cards Work in UAE (Quick Overview)

Understanding how credit cards work is important before comparing them with BNPL. In simple terms, a credit card gives you access to a revolving credit limit that you can use, repay, and reuse.

What Is a Credit Card?

A credit card allows you to borrow money from a bank to make purchases, with the agreement that you’ll repay it later.

- You get a credit limit (e.g., AED 10,000)

- You can spend up to that limit

- Once you repay, the limit becomes available again

This is called revolving credit, meaning there is no fixed end date—you can keep using the card as long as you manage repayments.

How Repayment Works

Every month, your bank generates a billing statement that shows:

- Total amount spent

- Minimum payment due

- Payment due date

You typically have two options:

- Pay the full amount → No interest is charged

- Pay the minimum amount (usually ~5%) → Remaining balance carries forward

👉 If you only pay the minimum, the rest of the balance continues into the next month.

How Interest Is Charged

Interest is only applied if you don’t pay the full statement amount by the due date.

- UAE credit cards usually charge around 2–4% per month on unpaid balances

- Interest is calculated daily, which means it can grow quickly over time

👉 Most UAE cards also offer an interest-free period of around 20–25 days.

However:

👉 If you don’t pay the full amount, you may lose this benefit, and interest can be charged from the original purchase date, not just after the due date.

What This Means for You

- Credit cards can be interest-free if used correctly (pay in full every month)

- But they can become expensive quickly if balances are carried forward

- The flexibility is useful—but it requires discipline

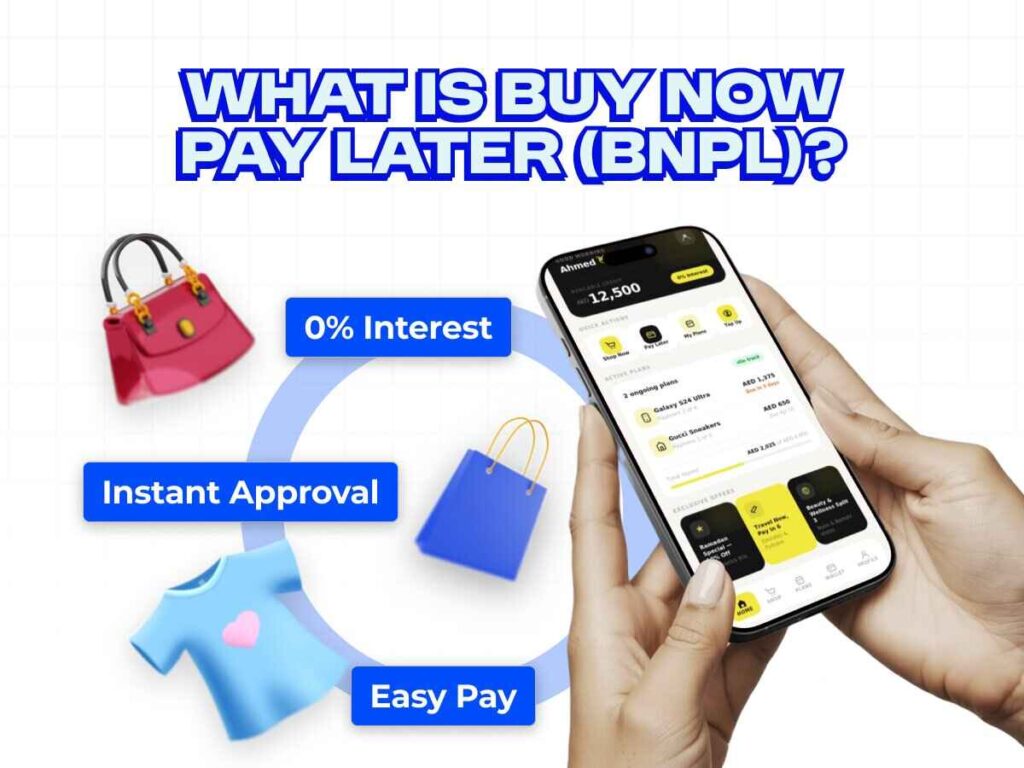

What Is Buy Now Pay Later (BNPL)?

Buy Now Pay Later (BNPL) is a payment option that allows you to split a purchase into smaller instalments instead of paying the full amount upfront.

It’s widely used across the UAE, especially for online shopping and retail purchases, and is designed for short-term, fixed repayment periods.

BNPL Explained Simply

With BNPL, you can:

- Buy a product today

- Pay a portion upfront (or sometimes nothing)

- Pay the remaining amount in 3–4 equal instalments over a few weeks or months

👉 For example:

If you buy something worth AED 1,000, you might pay AED 250 now and the rest in 3 equal payments.

Most BNPL providers in the UAE offer 0% interest if all payments are made on time, which is why it’s often seen as a low-cost alternative to credit cards.

How BNPL Repayments Work

BNPL follows a fixed repayment structure, unlike credit cards:

- Instalments are pre-defined at checkout

- Payments are automatically deducted from your card

- The repayment period is usually short-term (a few weeks to months)

👉 This means:

- You know exactly how much you owe and when

- There is a clear end date for the payment

Where BNPL Is Commonly Used in UAE

BNPL is widely available across the UAE, especially in:

- E-commerce platforms

- Fashion and lifestyle stores

- Electronics retailers

- Select in-store merchants and service providers

Many checkout pages now offer BNPL as a payment option, making it easy to use without a traditional credit card.

What This Means for You

- BNPL is now regulated as short-term credit in the UAE, which means it comes with real repayment obligations

- It can feel easier to manage because instalments are fixed

- But it is still not “free money”

If you want a deeper understanding of how BNPL works, including providers, eligibility, and benefits, check out our Complete Guide to Buy Now Pay Later (BNPL) in UAE.

BNPL vs Credit Card in UAE – Accessibility & Providers

One of the biggest differences between BNPL and credit cards in the UAE is how easy they are to access and who can actually get approved.

While both are forms of credit, the entry requirements, approval process, and usage scope are very different.

Eligibility Requirements for BNPL in UAE

BNPL is designed to be quick and easy to access, especially for everyday purchases.

Most providers typically require:

- Minimum age of 18

- UAE residency

- Valid Emirates ID

- Active mobile number

- A debit or credit card for repayments

👉 In many cases:

- Approval happens within minutes

- Only basic checks are done

- Some providers may review your payment history or credit data

This makes BNPL accessible to:

- Younger users

- New expats

- People without a strong credit history

👉 Also important:

BNPL providers in the UAE operate under Central Bank regulations, often through partnerships with licensed banks or finance companies.

Eligibility Requirements for Credit Cards in UAE

Credit cards have stricter requirements because they are long-term revolving credit products.

Typical requirements include:

- Minimum monthly salary (usually around AED 5,000 or more)

- Valid UAE residency and stable employment

- Acceptable credit score (AECB-based)

- Proof of income (salary certificate, bank statements)

👉 Banks also evaluate:

- Existing debts (debt burden ratio)

- Repayment capacity

Approval can take:

- Same day (in some cases)

- Or a few days with full verification

BNPL vs Credit Card – Which Is Easier to Get?

| Factor | BNPL | Credit Cards |

| Approval speed | Instant / minutes | Hours to days |

| Documentation | Minimal | Detailed |

| Salary requirement | Not strict | Usually ≥ AED 5,000 |

| Credit score requirement | Low / varies | Important for approval |

| Accessibility | High | Moderate to restrictive |

Popular BNPL Apps and Credit Card Providers in UAE

BNPL Providers in UAE

- Tabby

- Tamara

- Postpay

- Cashew

- Spotii

These are typically available at partner merchants or integrated checkout platforms.

Credit Card Providers in UAE

- Emirates NBD

- ADCB

- Mashreq

- FAB (First Abu Dhabi Bank)

- RAKBANK

These banks offer a wide range of cards with different:

- Limits

- Rewards

- Eligibility criteria

What This Means for You

- BNPL is easier to access, but limited to supported merchants and use cases

- Credit cards are harder to obtain, but offer universal acceptance and higher flexibility

👉 Your choice depends on your income, credit profile, and how widely you want to use the payment method

BNPL Fees vs Credit Card Interest – Which Is Cheaper?

When comparing BNPL and credit cards, the key question is:

👉 Which one actually costs less?

The answer depends entirely on how you use them—especially whether you pay on time or not.

BNPL Costs

Most BNPL services in the UAE are marketed as interest-free.

If you pay all instalments on time:

- 0% interest

- No standard processing fees (in most cases)

👉 This makes BNPL feel like a “free” way to split payments.

However, if you miss a payment:

- Late fees or collection charges may apply

- Your account may be restricted

- Repeated delays can impact your credit profile

👉 Important:

BNPL does not charge traditional interest, but it does include penalties for missed payments.

Also: In the UAE, BNPL fees are regulated and capped, meaning the total cost of a transaction cannot grow indefinitely.

Credit Card Costs

Credit cards can also be interest-free—but only if used correctly.

If you pay your full statement on time:

- No interest on purchases

But if you don’t:

- Interest is charged on the remaining balance

- UAE rates typically range from ~2–4% per month

- Interest is calculated daily and can compound over time

Additional costs may include:

- Annual fees

- Cash advance fees

- Late payment penalties

- Foreign transaction charges

👉 Unlike BNPL, there is no fixed cap on how much interest can accumulate over time.

Real-Life Cost Comparison (AED 1,000 Example)

Let’s say you buy a product worth AED 1,000.

| Scenario | BNPL | Credit Card |

| Paid on time | You pay AED 250 × 4 → Total = AED 1,000 | You pay full AED 1,000 → Total ≈ AED 1,000 (no interest if paid on time, excluding any card fees) |

| Miss 1 payment | Late fee (e.g., AED 20–50) → Total ≈ AED 1,020–1,050 | Interest (~3%) + late fee → Total ≈ AED 1,050–1,100 |

| Pay minimum only | Not applicable (fixed instalments) | Balance carries forward → interest keeps adding every month |

| Delay for 3–6 months | Fees increase but remain capped → Total stays limited | Interest compounds → Total can cross AED 1,200+ easily |

If you’re looking to reduce your overall spending, here are some proven ways to get maximum discounts in the UAE that can help you save even more on everyday purchases.

Short-Term vs Long-Term Cost Difference

- BNPL is designed for short-term use, with fixed repayment periods and bounded costs

- Credit cards are open-ended, where costs can increase significantly over time if balances are carried

👉 This is the biggest difference:

- BNPL → Predictable and capped

- Credit cards → Flexible but potentially unbounded

What This Means for You

- If you always pay on time, both options can be low-cost

- If you miss payments, credit cards can become much more expensive due to compounding interest

- BNPL is easier to predict, while credit card costs can grow silently over time

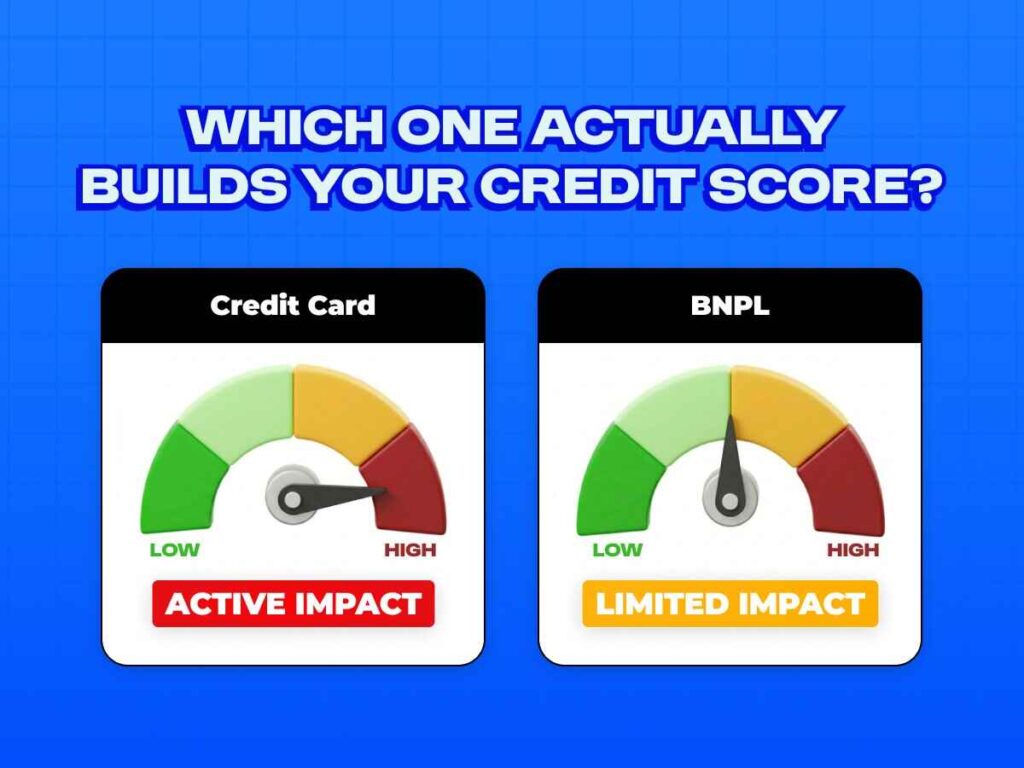

Credit Score Impact – BNPL vs Credit Cards

Your choice between BNPL and credit cards doesn’t just affect your spending—it can also impact your credit score in the UAE.

Understanding how each interacts with the Al Etihad Credit Bureau (AECB) is important, especially if you plan to apply for loans, mortgages, or higher-limit credit cards in the future.

Does BNPL Affect Credit Score in UAE?

BNPL is now increasingly treated as a form of short-term credit in the UAE.

- Some BNPL providers check your credit data before approval

- For higher-value transactions, providers may be required to consult AECB data

- Missed or repeated late payments can be reported to AECB

- Accounts may be restricted if repayments are delayed

👉 However:

- Not all providers consistently report on-time payments

- Positive credit-building impact is not yet standardized across providers

This means:

- BNPL can negatively affect your credit score if misused

- But it may not always help build your score significantly

How Credit Cards Affect Credit Score

Credit cards are fully integrated into the UAE’s credit system and have a direct and consistent impact on your AECB score.

Key factors include:

- Payment history → Paying on time improves your score

- Credit utilisation → Using too much of your limit can lower your score

- Account history → Long-term usage strengthens your profile

👉 Important:

- Late payments (especially beyond 30 days) can significantly reduce your score

- High balances relative to your limit can also negatively affect your profile

When used responsibly, credit cards are one of the most effective ways to build credit in the UAE

Which Option Builds Credit Better?

| Factor | BNPL | Credit Cards |

| Reporting to AECB | Partial / varies by provider | Fully integrated |

| Impact of on-time payments | Limited / unclear | Strong positive impact |

| Impact of missed payments | Can negatively affect score | Strong negative impact |

| Credit-building potential | Emerging | High |

What This Means for You

- If your goal is to build or improve your credit score, credit cards are more reliable

- If you use BNPL, treat it like real credit—missed payments can still affect your financial profile

- Don’t assume BNPL is “invisible” to the system anymore

👉 Also important: There is still limited public data on how consistently BNPL repayments improve credit scores in the UAE, so relying on it as a primary credit-building tool may not be effective.

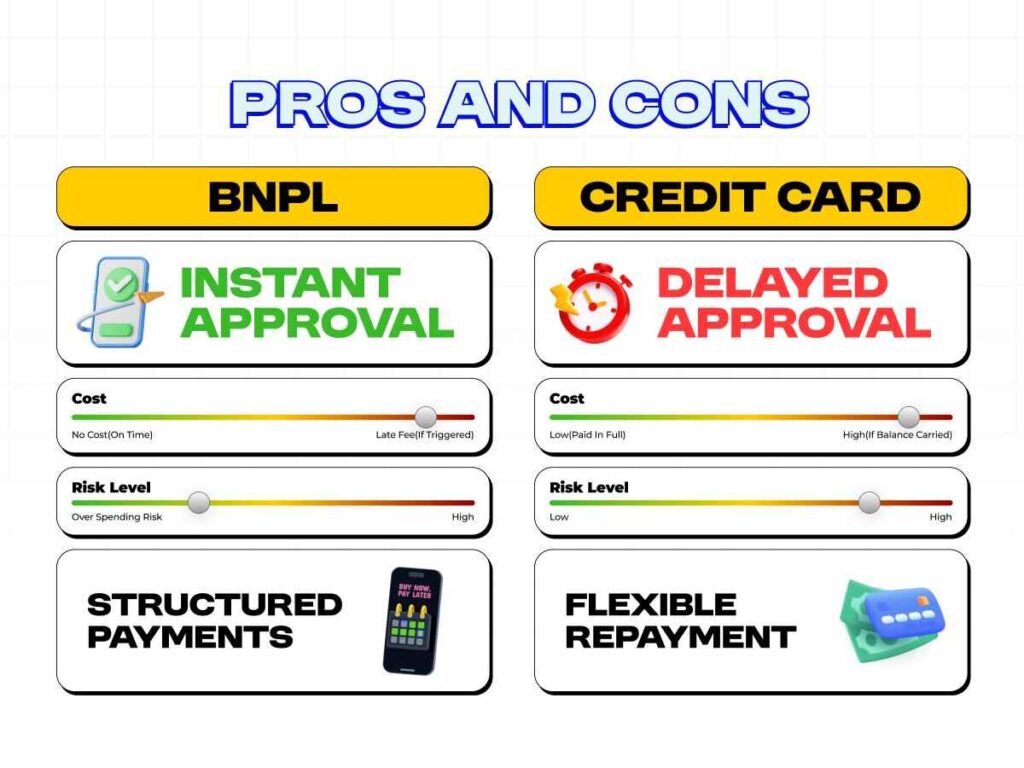

Pros and Cons of BNPL vs Credit Cards

Both BNPL and credit cards offer flexibility—but in very different ways. Understanding their advantages and drawbacks helps you choose based on your spending habits, discipline, and financial goals.

Advantages of BNPL

BNPL is designed for simplicity and short-term budgeting, which makes it appealing for controlled purchases.

- Interest-free instalments (if paid on time)

- Quick approval with minimal requirements

- Fixed repayment schedule with a clear end date

- Easier access for users with limited or no credit history

👉 This makes BNPL ideal for planned purchases where you want predictable payments without long-term commitments.

Disadvantages of BNPL

Despite its simplicity, BNPL comes with risks that are often underestimated.

- ❌ Overspending risk due to multiple active plans

- ❌ Late fees or penalties if payments are missed

- ❌ Limited to partner merchants and specific categories

- ❌ Less reliable for building long-term credit history

👉 Because instalments feel smaller, users often take multiple BNPL plans at once, which can make total spending harder to track.

Advantages of Credit Cards

Credit cards offer greater flexibility and long-term financial benefits when used responsibly.

- Widely accepted across UAE and globally

- Helps build credit history (AECB score)

- Offers rewards, cashback, and travel perks

- Useful for recurring expenses and emergencies

👉 This makes credit cards suitable for everyday spending, travel, and long-term financial planning.

Disadvantages of Credit Cards

Credit cards can become expensive and risky if not managed carefully.

- ❌ High interest rates on unpaid balances

- ❌ Risk of long-term debt due to revolving credit

- ❌ Multiple fees (annual, late payment, cash advance, etc.)

- ❌ Higher limits can encourage overspending

👉 The flexibility is powerful—but it requires strong repayment discipline.

What This Means for You

- BNPL often feels easier to control because payments are fixed and short-term

- Credit cards offer more power and flexibility, but also greater risk if balances are carried

👉 There’s no one-size-fits-all answer—the better option depends on how disciplined you are with repayments

When Should You Use BNPL vs Credit Card? (Decision Guide)

Choosing between BNPL and a credit card isn’t about which one is “better”—it’s about which one fits your situation.

The right choice depends on:

- The type of purchase

- Your repayment ability

- Your credit goals

- Your spending habits

Use BNPL If

BNPL is better suited for short-term, specific purchases where you want structure and predictability.

You should consider BNPL when:

- You’re making a one-time purchase (e.g., electronics, fashion, furniture)

- The merchant offers BNPL at checkout

- You want fixed instalments with a clear end date

- You want to avoid long-term revolving debt

- You don’t have a credit card or prefer not to use one

👉 BNPL works best when:

- You are confident you can pay all instalments on time

- You are managing only a limited number of plans

- The purchase fits within your short-term budget

Use Credit Card If

Credit cards are better for flexibility, broader usage, and long-term financial benefits.

You should consider a credit card when:

- You need wide acceptance (travel, bills, emergencies)

- You want to earn rewards, cashback, or air miles

- You are making frequent or recurring payments

- You want to build or improve your credit score

- You can pay the full balance every month

👉 Credit cards are ideal for:

- Everyday expenses (groceries, fuel, subscriptions)

- Travel bookings and international transactions

- Emergency situations where BNPL may not be available

You May Like This : Best UAE credit card offers for flight ticket discounts you can take advantage of.

Quick Decision Guide

| Scenario | Better Option | Why |

| Buying a mid-range gadget from a BNPL-enabled store | BNPL | Fixed instalments, no interest if paid on time |

| Booking flights or hotels | Credit Card | Wider acceptance + travel benefits |

| Everyday expenses (groceries, fuel) | Credit Card | Rewards + monthly consolidation |

| New to UAE / no credit history | BNPL | Easier approval and access |

| Emergency expense | Credit Card | Immediate access and higher limits |

| One-time planned purchase with clear repayment ability | BNPL | Structured short-term repayment |

👉 The key is not choosing one over the other—but using each tool in the right situation

Shopping Tip: If you frequently shop at Noon and plan to use BNPL or a credit card, it’s worth checking QYUBIC first for extra savings.

Conclusion – Making Smarter Payment Decisions in UAE

BNPL and credit cards aren’t competing choices—they’re tools designed for different situations.

The real advantage comes from how you use them, not which one you pick.

In the UAE’s growing digital payment landscape, it’s becoming easier than ever to split payments, access credit, and shop more conveniently. But that convenience also makes it easier to overlook the true cost of spending.

FAQs

1. Can you use BNPL for essentials like groceries or rent in UAE?

BNPL is mostly limited to partner merchants, so it’s commonly used for shopping categories like fashion, electronics, and lifestyle products.

It is generally not available for rent, utilities, or most everyday essential payments, unlike credit cards.

2. What happens if you miss multiple BNPL payments at the same time?

If you have multiple active BNPL plans and miss payments:

- Late fees may apply on each plan

- Your account can be restricted

- Future purchases may be blocked

👉 More importantly, repeated missed payments may now impact your credit profile, especially under UAE’s evolving credit regulations.

3. Is BNPL Sharia-compliant in the UAE?

Some BNPL providers structure their services to align with Islamic finance principles, mainly because they do not charge traditional interest.

However, compliance can vary by provider, so users should check specific terms and certifications if this is important to them.

4. Can you use BNPL and credit cards together for the same purchase?

In most cases, BNPL requires a debit or credit card for repayment, but you cannot typically split a single transaction between BNPL and a credit card at checkout.

👉 However, you may still indirectly use both—for example: Using a credit card as the repayment method for BNPL instalments

5. Does cancelling a BNPL order affect your credit score?

Cancelling an order usually does not affect your credit score, as long as:

- The cancellation is processed before payments are due

- There are no missed instalments

👉 Issues arise only if payments are delayed or skipped.

6. Why do some BNPL transactions get declined even if you qualify?

Even if you meet basic eligibility, BNPL approvals are based on:

- Your past repayment behavior

- Current outstanding BNPL plans

- Risk checks by the provider

👉 This means approvals are dynamic, not guaranteed.