Ever wondered if the best credit card for points and travel actually lives up to the hype? You’re not alone. Globally, people earned over $41 billion in credit card rewards in a single year, yet many still struggle to extract real value from them. While millions search for the best credit card for travel points, the reality is far more complex. This guide breaks it down simply so you can finally decide what the best credit card for travel points is for your lifestyle, not just on paper.

Best Credit Card for Travel Point (Quick Snapshot)

| Category | Card Name | Key Highlights |

Best Overall Travel Rewards (Flexible Points) | Citi Prestige | Flexible airline transfers, 4th night free hotel, unlimited lounge access |

| Standard Chartered Journey | Strong miles earning, unlimited lounge + guest, airport transfers | |

| Mashreq Solitaire | High earning rate on travel, premium perks, and flexible redemption | |

Best Premium Travel Card (Luxury Benefits) | American Express Platinum UAE | Elite hotel status, global lounge collection, premium concierge |

| Citi Ultima | High miles earning, 50% flight rebate, luxury travel perks | |

| Emirates Islamic Skywards Black | Fast-track Emirates Gold, high Skywards earning, premium travel benefits | |

Best Low Annual Fee Travel Card | RAKBANK Air Arabia Platinum | Low fee, Air Arabia rewards, free flight voucher |

| HSBC Skywards Signature | Easy Emirates miles earning, Silver status fast-track | |

| CBD One Credit Card | Customizable benefits, flexible rewards, and optional lounge access | |

Best for Lounge Access | HSBC Premier Credit Card | Unlimited lounge access, no annual fee (for Premier users) |

| CBD Visa Infinite | Unlimited lounge + guest, strong welcome cashback | |

| Emirates NBD dnata Platinum | Travel-focused rewards, lounge access, and dnata redemption |

Best Credit Cards for Points and Travel

Explore the best credit card for points and travel options designed to help you earn smarter, redeem efficiently, and maximize real travel value without unnecessary complexity or hidden limitations

Best Overall Travel Rewards Card (Flexible Points)

Citi Prestige

The Citi Prestige Credit Card is the top-tier best travel credit card in the UAE for high-net-worth frequent flyers seeking luxury perks.

- Best for: Luxury travelers seeking hotel benefits and flexible air miles transfers.

- Annual Fee: AED 1,500.

- Welcome Bonus: AED 750 statement credit (spend AED 20,000 within 90 days) plus 10,000 annual renewal points.

- Rewards Earning: 3 ThankYou Points per $1 spent internationally; 2 points locally.

- Points/Miles Type: Citi ThankYou Points (never expire).

- Redemption Options: Transfer to 12+ partners (Etihad, Emirates, British Airways) or cash rebates.

- Travel Perks: Complimentary 4th night free at any hotel worldwide and unlimited golf.

- Lounge Access: Unlimited global access for the cardholder plus one guest via Mastercard Travel Pass.

- Foreign Transaction Fee: 2.99%.

- Eligibility: Minimum monthly income of AED 30,000.

- Pros: Unmatched hotel “4th night free” value; diverse airline transfer partners.

- Cons: High non-waivable fee; steep minimum income requirement.

Standard Chartered Journey Credit Card

The Standard Chartered Journey Credit Card is a powerhouse for frequent flyers in the UAE, designed to turn everyday spending into premium travel experiences.

- Best for: Travelers prioritizing flexible air miles and comprehensive airport lounge access.

- Annual Fee: AED 1,575 (Waived in year 1 if you spend AED 10,000 within 60 days).

- Welcome Bonus: Up to AED 1,000 cashback for new successful applications.

- Rewards Earning: 4 360° Rewards points per $1 on international spends; 2 points per $1 locally.

- Points/Miles Type: 360° Rewards Points.

- Redemption Options: Transfer to major partners like Emirates Skywards and Etihad Guest, or redeem for cashback and e-vouchers.

- Travel Perks: 4 complimentary airport transfers via Careem (promo code: SCB100) and 10% cashback at UAE Duty Free.

- Lounge Access: Unlimited access to 1,000+ lounges for the cardholder and one guest via the Visa Airport Companion app.

- Foreign Transaction Fee: Standard rates apply (look for seasonal 3% cashback offers on international POS).

- Eligibility: Minimum monthly income of AED 30,000.

- Pros: Strong miles transfer flexibility; unlimited lounge guest access; easy first-year fee waiver.

- Cons: High income requirement; duty-free/Careem perks require a prior airline transaction.

Mashreq Solitaire Credit Card

The Mashreq Solitaire Credit Card is a premier status symbol for high-earning residents, blending luxury lifestyle perks with robust travel rewards.

- Best for: High-spenders seeking premium lifestyle benefits like golf, fitness, and luxury travel insurance.

- Annual Fee: AED 1,500 (+ 5% VAT).

- Welcome Bonus: Up to AED 2,500 cashback for new customers (spend AED 9,000 within the first 2 months).

- Rewards Earning: 6 Mashreq Vantage points per AED on international spend; 4 points on airlines/hotels; 2 points locally.

- Points/Miles Type: Mashreq Vantage Points (formerly Salaam Points).

- Redemption Options: Instant redemption via the Mashreq Mobile App for air miles, gift cards, or cashback.

- Travel Perks: 6 complimentary airport transfers annually and unlimited Fitness First visits.

- Lounge Access: Unlimited access to 1,000+ lounges for cardholder + guest (requires 1 international transaction annually).

- Foreign Transaction Fee: Approximately 2.89%.

- Eligibility: Minimum monthly salary of AED 25,000.

- Pros: Massive welcome bonus; unlimited fitness and valet perks; flexible point redemptions.

- Cons: High annual fee; specific benefits (golf/valet) require a minimum monthly spend of AED 10,000.

Best Premium Travel Card (Luxury Benefits)

American Express Platinum Card UAE

The American Express Platinum Card UAE is the ultimate best travel credit card in the UAE for high-end globetrotters seeking unmatched elite status and concierge services.

- Best for: Ultra-high-net-worth travelers who value elite hotel status and worldwide lounge access over simple cashback.

- Annual Fee: AED 2,625 (roughly $715).

- Welcome Bonus: Often 25,000 to 50,000 Membership Rewards points (subject to seasonal Amex UAE offers).

- Rewards Earning: 1 Membership Rewards Point for every $1 spent; higher tiers for specific categories via “Reward Multiplier.”

- Points/Miles Type: Membership Rewards (MR) Points.

- Redemption Options: Transfer to 10+ airlines (Emirates, Etihad, Qatar) and hotels (Marriott, Hilton) at competitive ratios.

- Travel Perks: Complimentary Elite Status (Marriott Bonvoy Gold, Hilton Honors Gold), Fine Hotels & Resorts benefits, and comprehensive travel insurance.

- Lounge Access: Unlimited access to 1,400+ lounges, including The Centurion Lounge, Priority Pass, and Delta Sky Clubs.

- Foreign Transaction Fee: 2.8% on non-USD/AED transactions.

- Eligibility: High minimum income (typically AED 35,000+ monthly) and strict credit history.

- Pros: Unrivaled “Global Lounge Collection”; instant elite hotel status; premium 24/7 concierge.

- Cons: Highest annual fee in its class; lower points earning rate than some competitors.

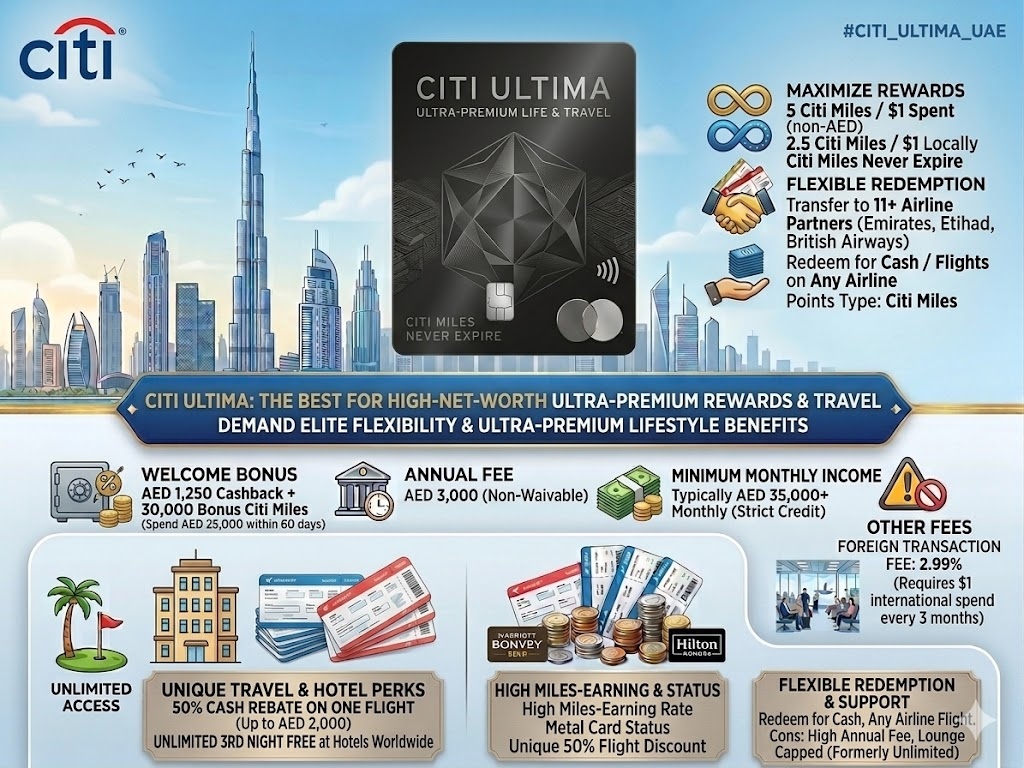

Citi Ultima Credit Card

The Citi Ultima Credit Card is widely considered the best credit card for points and travel in the UAE for high-net-worth individuals who demand elite flexibility and ultra-premium lifestyle benefits.

- Best for: Ultra-high spenders seeking a metal card with flexible air mile transfers and “buy one, get one” flight deals.

- Annual Fee: AED 3,000.

- Welcome Bonus: AED 1,250 cashback (spend AED 25,000 within 60 days) plus 30,000 bonus Citi Miles annually.

- Rewards Earning: 5 Citi Miles per $1 on non-AED spend; 2.5 Citi Miles per $1 locally.

- Points/Miles Type: Citi Miles (never expire).

- Redemption Options: Transfer to 11+ partners (Emirates, Etihad, British Airways) or redeem for cash/flights on any airline.

- Travel Perks: 50% cash rebate on one flight ticket annually (up to AED 2,000) and unlimited 3rd night free at hotels worldwide.

- Lounge Access: 14 complimentary visits per year via Mastercard Travel Pass (requires $1 international spend every 3 months).

- Foreign Transaction Fee: 2.99%.

- Eligibility: Minimum monthly income of AED 35,000.

- Pros: High miles-earning rate; metal card status; unique 50% flight discount.

- Cons: High annual fee; lounge access is capped (formerly unlimited).

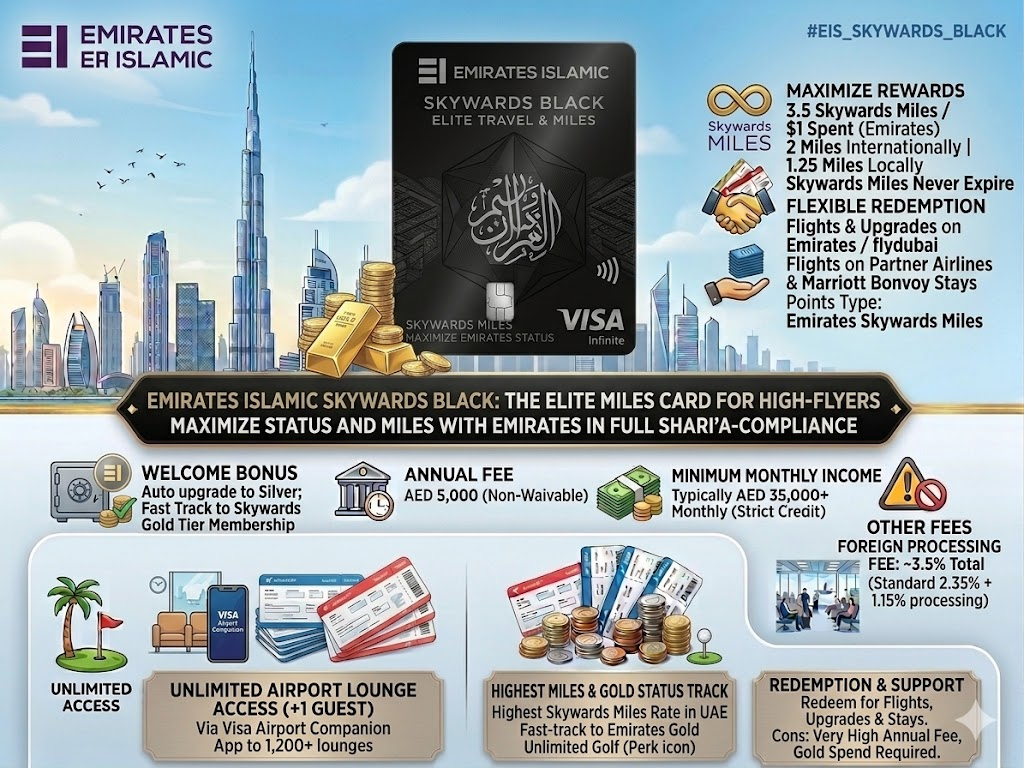

Emirates Islamic Skywards Black Credit Card

The Emirates Islamic Skywards Black Credit Card is an elite Shari’a-compliant card designed for high-flyers who want to maximize their status and miles with Emirates.

- Best for: Ultra-frequent Emirates travelers seeking a fast track to Gold status and high-mile earnings.

- Annual Fee: AED 5,000.

- Welcome Bonus: Automatic upgrade to Emirates Skywards Silver and a fast track to Gold Tier Membership.

- Rewards Earning: Up to 3.5 Skywards Miles per $1 on Emirates spend; up to 2 miles internationally, and 1.25 miles locally.

- Points/Miles Type: Emirates Skywards Miles.

- Redemption Options: Flights and upgrades with Emirates/flydubai, partner airlines, or Marriott Bonvoy stays.

- Travel Perks: 4 complimentary airport transfers annually and 25% discount on “Buy Miles.”

- Lounge Access: Unlimited complimentary access to 1,200+ lounges for the cardholder plus one guest via Visa Airport Companion.

- Foreign Transaction Fee: Standard 2.35% plus 1.15% processing fee (approx. 3.5% total).

- Eligibility: Minimum monthly income of AED 35,000.

- Pros: Fast-track to Emirates Gold; highest Skywards miles rate in the UAE; unlimited golf.

- Cons: Very high annual fee; specific spend requirements to maintain Gold status.

Best Low Annual Fee Travel Card

RAKBANK Air Arabia Platinum Credit Card

The RAKBANK Air Arabia Platinum Credit Card is the best travel credit card in the UAE for budget-conscious frequent flyers who prefer low-cost carriers without sacrificing premium perks.

- Best for: Families and frequent regional travelers using Air Arabia for value-driven trips.

- Annual Fee: AED 400 (Waived for the first year).

- Welcome Bonus: Up to 300 Air Rewards points (joining bonus) plus a complimentary return flight voucher.

- Rewards Earning: 1.75 Air Rewards points per AED 5 on international spend; 1.25 points locally; 2.75 points on Air Arabia.

- Points/Miles Type: Air Arabia Air Rewards.

- Redemption Options: Flexible “Cash + Points” for flights, baggage, and meals with no blackout dates.

- Travel Perks: Complimentary excess baggage (up to 30kg) and 0% interest payment plans for Air Arabia bookings.

- Lounge Access: Unlimited access to 10+ regional lounges in the Middle East via Mastercard For You.

- Foreign Transaction Fee: 2.95%.

- Eligibility: Minimum monthly income of AED 10,000.

- Pros: Low entry barrier; high rewards for budget travel; excellent baggage benefits.

- Cons: Limited to Air Arabia network; fewer luxury lifestyle perks compared to premium cards.

HSBC Emirates Skywards Signature Credit Card

The HSBC Emirates Skywards Signature Credit Card is a balanced choice for the best travel credit cards in the UAE, offering an entry point to Emirates elite status and miles.

- Best for: Frequent Emirates flyers seeking a fast track to Silver status with a moderate income requirement.

- Annual Fee: AED 1,050.

- Welcome Bonus: Up to 25,000 Skywards Miles (10,000 on fee payment + 15,000 after spending AED 20,000 in 60 days) and a fast track to Silver Tier status.

- Rewards Earning: Up to 1.75 Skywards Miles per $1 on Emirates/flydubai; 1.25 on international; 1.0 locally.

- Points/Miles Type: Emirates Skywards Miles (non-expiring).

- Redemption Options: Flights, upgrades, and partner rewards via Emirates Skywards.

- Travel Perks: Complimentary subscription to Careem+, discounts on Amazon, and Airalo international roaming.

- Lounge Access: 12 complimentary visits annually to 1,200+ lounges via the Visa Airport Companion app.

- Foreign Transaction Fee: Approximately 3.1%.

- Eligibility: Minimum monthly income of AED 10,000.

- Pros: Easy fast-track to Silver status; non-expiring miles; useful local lifestyle discounts.

- Cons: Higher foreign transaction fees compared to competitors; low earning rates on specific categories like supermarkets.

CBD One Credit Card

The CBD One Credit Card by Commercial Bank of Dubai is a unique, customizable best credit card for points and travel in the UAE, allowing users to “design” their own benefits via the CBD app.

- Best for: Tech-savvy travelers who want to pay only for the specific perks they use.

- Annual Fee: Monthly subscription model (ranges from AED 0 to AED 250 depending on the chosen tier/benefits).

- Welcome Bonus: Up to AED 1,000 cashback (conditional on monthly spend targets).

- Rewards Earning: Up to 2.5 CBD Rewards points per AED 1 spent on international transactions; 1.5 points locally.

- Points/Miles Type: CBD Rewards Points.

- Redemption Options: Flexible redemptions for flights, hotels, gift cards, or instant cashback via the app.

- Travel Perks: Custom choice of multi-trip travel insurance, 0% Easy Payment Plans, and Careem discounts.

- Lounge Access: Up to unlimited access to 1,000+ lounges via LoungeKey (tiered based on selected plan).

- Foreign Transaction Fee: Competitive rates around 1.99% to 2.85% depending on the tier.

- Eligibility: Minimum monthly income of AED 10,000.

- Pros: Total flexibility; transparent monthly pricing; high points earning on international spend.

- Cons: Premium features require higher monthly fees; rewards can be complex to optimize.

Best Credit Cards for Lounge Access

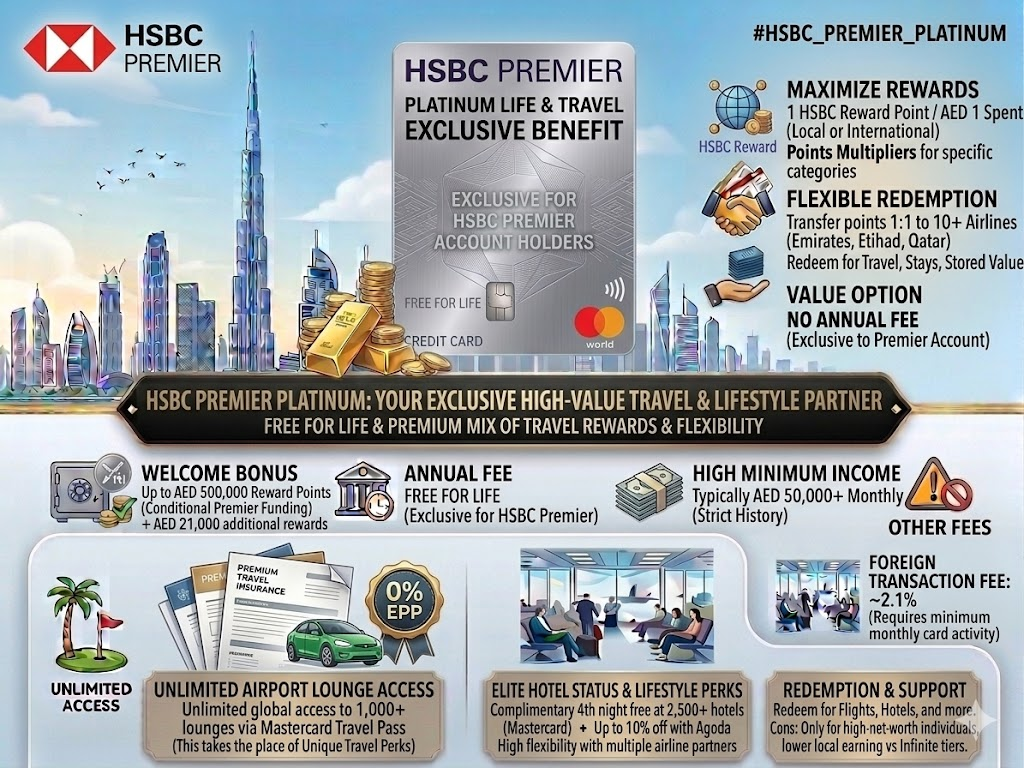

HSBC Premier Credit Card

The HSBC Premier Credit Card is an exclusive benefit for HSBC Premier banking customers, offering a premium mix of travel rewards and lifestyle flexibility.

- Best for: Existing HSBC Premier customers who want a high-value travel card with no additional annual cost.

- Annual Fee: Free for life (exclusive to HSBC Premier account holders).

- Welcome Bonus: Up to AED 500,000 reward points (conditional on Premier account funding) and up to AED 21,000 in additional rewards.

- Rewards Earning: 1 HSBC Reward Point for every AED 1 spent locally or internationally.

- Points/Miles Type: HSBC Air Miles or Reward Points.

- Redemption Options: Transfer points 1:1 to airline partners like Emirates Skywards, British Airways Executive Club, and Singapore Airlines KrisFlyer.

- Travel Perks: Complimentary 4th night free at over 2,500 hotels via Mastercard and up to 10% off with Agoda.

- Lounge Access: This credit card is known for Unlimited lounge access to 1,000+ lounges globally for the cardholder via Mastercard Travel Pass.

- Foreign Transaction Fee: Competitive at approximately 2.1%.

- Eligibility: Must be an HSBC Premier customer (requires a monthly salary of AED 50,000+ or TRB of AED 350,000+).

- Pros: No annual fee for Premier members; high flexibility with multiple airline partners; elite hotel status perks.

- Cons: Only accessible to high-net-worth individuals; local earning rate is lower than some dedicated “Infinite” tier cards.

CBD Visa Infinite Credit Card

The CBD Visa Infinite Credit Card is a premium, best travel credit card in the UAE designed for high-earning individuals who want top-tier exclusivity and reward flexibility.

- Best for: Luxury seekers and frequent travelers looking for a high cashback welcome offer and lifestyle perks.

- Annual Fee: AED 750 (often waived for the first year or for specific account tiers).

- Welcome Bonus: Up to AED 2,000 cashback for new customers who spend AED 12,000 within 30 days.

- Rewards Earning: Up to 3 CBD Rewards Points per AED 1 spent.

- Points/Miles Type: CBD Rewards Points.

- Redemption Options: Redeem points for Skywards Miles, cashback, or various retail vouchers via the CBD App.

- Travel Perks: Up to 12% off Agoda, 8% off Booking.com, and comprehensive multi-trip travel insurance.

- Lounge Access: Unlimited global access to 1,000+ lounges for the cardholder plus one guest via the Visa Airport Companion App.

- Foreign Transaction Fee: Standard rates (approx. 2.85%) apply.

- Eligibility: Minimum monthly salary of AED 25,000.

- Pros: Massive AED 2,000 sign-up bonus; 4 free rounds of golf monthly; 50% off cinema tickets.

- Cons: High spend requirement for the welcome bonus; eligibility restricted to high-income earners.

Emirates NBD dnata Platinum Credit Card

The Emirates NBD dnata Platinum Credit Card is a top contender for the best travel credit card in the UAE, offering flexible travel rewards through the dnata network.

- Best for: Residents seeking high rewards on dnata travel bookings and duty-free shopping.

- Annual Fee: AED 525.

- Welcome Bonus: Travel vouchers worth up to AED 2,500 upon card activation.

- Rewards Earning: Up to 15% back in dnata Points on purchases at dnata Travel, World Duty Free, and select outlets.

- Points/Miles Type: dnata Points (1 Point = AED 1).

- Redemption Options: Instant redemption for flights, hotel stays, or holiday packages at dnatatravel.com or in-store.

- Travel Perks: 0% interest installment plans for dnata Travel and school fees; “buy one, get one free” cinema tickets at Reel Cinemas.

- Lounge Access: Complimentary access to 1,000+ airport lounges globally via the Mastercard Travel Pass app.

- Foreign Transaction Fee: 1.99%.

- Eligibility: Moderate minimum income requirement (typically AED 10,000–15,000 monthly).

- Pros: High reward rate for travel; transparent 1:1 point-to-dirham value; zero foreign transaction fee promos often available.

- Cons: High APR (41.88%); points are primarily restricted to the dnata ecosystem.

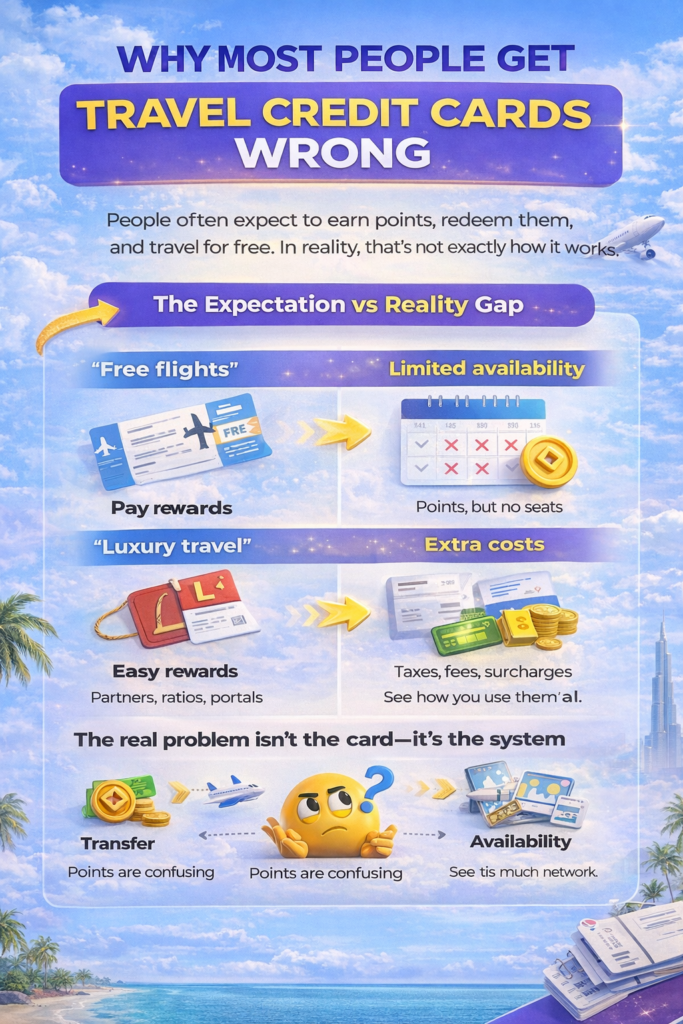

Why Most People Get Travel Credit Cards Wrong

Most people searching for the best credit card for flight discounts or points are not making a bad choice—they are starting with the wrong expectations.

On the surface, travel credit cards look simple:

👉 earn points → redeem → travel for free

But in reality, it works very differently.

The expectation vs reality gap

This is where most frustration begins.

- “Free flights” → Limited availability You may have enough points, but not the seats—especially during holidays or fixed travel dates.

- “Luxury travel” → Extra costs: Taxes, fuel surcharges, and fees can turn a “free” ticket into a costly one.

- “Easy rewards” → Complex systems. Instead of one simple process, you deal with the following:

- airline partners

- transfer ratios

- booking portals

- airline partners

👉 This is why many people who look for the best credit card for travel points feel disappointed later.

The real problem isn’t the card—it’s the system

Here’s what most people don’t know:

- You often need to go through multiple steps:

card → transfer → airline → availability → booking - Rules keep changing

Points lose value, benefits change, and what worked last year may not work today - Hidden constraints matter more than points

- limited award seats

- fixed travel dates

- Family bookings needing multiple seats

- limited award seats

👉 So when people ask, “What is the best credit card for travel points?”

The real answer depends on whether they can handle the system behind it.

How Travel Credit Cards Actually Work (Simplified)

If you’re trying to find the best credit card for points and travel, here’s the truth most people miss:

👉 The system has three layers — earning, redeeming, and value — and each one works differently.

Step 1: Earn points

At the most basic level, travel cards reward you for spending.

- You earn points or miles on every purchase

- Some categories (travel, lounge access, online spending) give higher rewards

But here’s what people don’t realize:

- Rewards depend on how transactions are categorized

- Bonus points only trigger if the purchase matches specific categories

👉 This is why even the best credit card for travel points may not always give expected rewards.

Step 2: Redeem points (3 main ways)

This is where the real difference happens.

1. Travel portal (easy, moderate value)

- Book flights and hotels directly through the card platform

- Works like a normal booking site

- Simple, but not always the highest value

2. Transfer to partners (complex, highest potential value)

- Move points to airline or hotel programs

- Can unlock 2x higher value or more in some cases

- Requires planning, timing, and availability

3. Cashback/statement credit (simplest, lowest value)

- Converts points into money

- Easy to use, but typically gives lower returns per point

Step 3: Why is the value inconsistent

This is the biggest confusion point.

👉 The same points can have completely different value.

It depends on:

- Timing—prices and availability change constantly

- Availability—award seats may not exist even if you have points

- Redemption method—portal vs transfer can change value significantly

For example, the same points might give

- ~0.5–1 value via cashback

- ~1–1.5 via portals

- ~2+ via partner transfers

The Biggest Problems With Travel Points (A Reality Check)

Before you pick the best credit card for points and travel, you need to understand where most people struggle.

Travel rewards are powerful—but only if you can navigate the friction behind them.

Let’s break this down into what actually goes wrong.

1. Redemption is more complex than it looks

Earning points is easy. Using them well is not.

- Booking often involves multiple steps: search → transfer → partner → book

- Airline partners and transfer ratios vary, making comparisons confusing

- There’s a real learning curve to get good value

👉 This is why many people never fully use the benefits of the best credit card for travel points.

2. Availability is the real bottleneck

Even if you have enough points, you may not be able to use them.

- No award seats during peak travel (holidays, school breaks)

- Difficult for families needing multiple seats

- Business and first-class seats are limited

👉 Points don’t guarantee travel—availability does.

3. Points are risky assets

Most people treat points like money. They’re not.

- Programs can devalue points anytime

- Transfers are usually irreversible

- Points can expire if unused

👉 Holding points too long can reduce their value significantly.

4. Annual fees are hard to justify

Premium cards look attractive—but reality is different.

- Benefits often feel like a “coupon book.”

- Break-even is unclear

- Infrequent travelers don’t use enough perks

👉 A high-fee card is only worth it if you use it consistently.

5. Portals vs transfers create confusion

This is one of the biggest decision gaps.

- Travel portals may show higher prices

- Not all flights/hotels appear (limited inventory)

- Booking through portals may block loyalty benefits

👉 What looks easier isn’t always better.

6. Hidden value leaks most people ignore

Even good redemptions lose value due to small details:

- Taxes and fuel surcharges on “free” flights

- Foreign transaction fees when traveling abroad

- Bonus categories not triggering due to MCC issues

- Travel insurance that’s hard to claim due to fine print

Travel Points vs. Cash Back — What’s Actually Better?

Before choosing the best credit card for points and travel, you need to answer one simple question: Do you want maximum value or maximum simplicity?

Because that’s what this really comes down to.

| Factor | Travel Points | Cash Back |

| Ease of Use | Complex—requires understanding partners, transfers, and booking strategies | Very simple—earn and redeem as money |

| Value Potential | High (can be 2x–5x in some cases with optimization) | Fixed (usually 1%–5%) |

| Flexibility | Limited — depends on airlines, hotels, and availability | Very high — can use anywhere |

| Best For | Frequent travelers, flexible planners, optimization mindset | Beginners, low-frequency travelers, simplicity seekers |

| Redemption Process | Multi-step (search → transfer → book) | One-step (redeem anytime) |

| Risk Factor | High—devaluation, expiry, transfer mistakes | Low value is stable and predictable |

| Availability Issues | Common — especially during peak dates or for families | None — no restrictions |

| Time Investment | High — requires research and tracking | Minimal — no learning curve |

| Premium Perks | Strong — lounge access, upgrades, travel benefits | Limited — mostly basic rewards |

| Hidden Costs | Taxes, surcharges, forex fees, missed multipliers | Almost none |

| Annual Fee Justification | Harder — depends on usage of perks and travel frequency | Easier — rewards are straightforward |

How to Know if a Travel Credit Card Is Worth the Annual Fee

Choosing the best credit card for points and travel is not about premium features—it’s about real value. Here’s how to evaluate it properly:

- Start with a realistic break-even calculation

Always compare the annual fee against what you will actually use, not the total advertised benefits. Most users overestimate value at this stage. - Only count credits you naturally use

Travel credits, dining credits, or vouchers only add value if they match your real spending habits. Forced usage does not count as savings. - Estimate rewards conservatively, not optimistically

Do not assume the maximum point value. Use the average redemption value, because most users don’t optimize transfers or find high-value redemptions consistently. - Check how often you will use lounge access

Lounge access looks attractive, but if you travel only a few times a year, its real value becomes negligible. - Evaluate if perks fit your lifestyle

Benefits like hotel status or concierge services only matter if you actually use them. Otherwise, they inflate perceived value without real returns. - Consider your travel frequency honestly

If you are not traveling regularly, even the best credit card for travel points will struggle to justify a high annual fee. - Account for hidden value leaks

Forex fees, taxes on award bookings, and unused benefits can quietly reduce your total return, making the card less valuable than expected.

At Last

There is no single best credit card for travel points—and that’s the honest truth. The right choice depends on how you actually travel and spend. Beginners are better off with simple or low-fee options, while frequent travelers can unlock more value from flexible points systems. For most people, the best credit card for points and travel is the one they can use consistently without complexity. Travel rewards are powerful—but only when they match your real habits, not unrealistic expectations.

If you want to reduce your flight booking expenses, platforms like the QYUBIC Coupon & Discount Platform offer handpicked deals, promo codes, and exclusive discounts to help you save more on airfare.