If you’ve been shopping online in the UAE recently, chances are you’ve seen options like “Pay in 4,” “Pay later,” or “Split your payment” at checkout.

That’s Buy Now Pay Later (BNPL) — and it’s quickly becoming one of the most popular ways to pay in the UAE.

From booking flights and buying the latest iPhone to ordering groceries or even paying for healthcare, BNPL is now everywhere. And there’s a reason for that.

With a mobile-first population, booming e-commerce market, and strong demand for flexible payments, BNPL has gone from a niche payment method to a mainstream financial tool.

But here’s the thing:

👉 BNPL is simple to use — but it’s still a form of credit.

So before you start using it regularly, it’s important to understand:

- How it works

- Where you can use it

- Which providers are best

- And how to use it responsibly

Let’s break it all down.

What is Buy Now Pay Later (BNPL)? Why is it Growing in Popularity in the UAE?

What is BNPL? (Simple Explanation)

Buy Now Pay Later (BNPL) is a short-term financing option that allows you to:

- Purchase a product or service immediately

- Pay for it over time in fixed installments

Most BNPL plans follow this structure:

| Feature | Description |

| Payment type | Installments |

| Interest | Usually 0% (if paid on time) |

| Duration | 2 weeks to 24 months |

| Approval | Instant or near-instant |

| Payment method | Debit or credit card |

How BNPL Works (Behind the Scenes)

Here’s what actually happens:

- You select BNPL at checkout

- The BNPL provider pays the merchant upfront

- You repay the provider in installments

- Payments are automatically deducted

BNPL vs Credit Cards vs Loans (Critical Difference)

| Feature | BNPL | Credit Card | Personal Loan |

| Interest | Usually 0% | High interest if balance is carried beyond due date (often 20–40% APR) | Moderate |

| Approval | Instant | Requires application, credit assessment, and approval | Slow |

| Structure | Fixed installments | Revolving credit with minimum payment option | Fixed EMI |

| Usage | Merchant-specific | Accepted widely across online and offline merchants | Disbursed as a lump sum for general use |

| Paperwork | Minimal (basic details and verification) | Moderate (KYC + income/credit checks) | Extensive (documentation, income proof, credit checks) |

Why BNPL is Growing Rapidly in the UAE

1. Massive Digital & Mobile Penetration

This is particularly evident in urban centers like Dubai and Abu Dhabi, where mobile-first shopping is already the norm.

- ~99% internet penetration

- ~96% smartphone ownership

- Mobile-first shopping behavior

👉 BNPL fits perfectly into this ecosystem.

2. Explosive E-commerce Growth

Cities like Dubai and Abu Dhabi lead this growth, with higher online spending across electronics, fashion, and travel.

- UAE e-commerce market is projected to exceed AED 48+ billion

- Categories like electronics, fashion, and travel dominate

BNPL directly boosts:

- Cart size

- Conversion rates

3. Strong Adoption Among Millennials & Gen Z

BNPL users are primarily:

- Aged 20–40

- Digitally fluent

- Prefer flexibility over long-term debt

4. Preference for Interest-Free Finance

In the UAE:

- Credit cards often carry high interest rates

- BNPL offers transparent, interest-free payments

5. Lifestyle & High-Value Spending

BNPL thrives in categories like:

- Travel

- Electronics

- Luxury goods

Because it transforms: AED 4,000 purchase → AED 1,000 installments

6. Accessibility for Expats

Unlike traditional credit:

- BNPL requires minimal credit history

- Works well for UAE’s expatriate population

Benefits of Using BNPL in the UAE

BNPL may look like a simple payment option at checkout, but its impact is more practical than it seems.

Instead of paying everything upfront, you’re effectively restructuring your spending over time, which can make a noticeable difference in how you manage purchases.

Here are the key benefits that explain why more people are using it.

1. Flexible Payment Structure

Instead of paying a large amount upfront:

| Example Purchase | Without BNPL | With BNPL |

| AED 4,000 laptop | Pay AED 4,000 now | Pay AED 1,000 × 4 |

👉 Makes high-value purchases manageable.

2. Interest-Free Payments

Most UAE BNPL providers offer:

- 0% interest

- No hidden charges (if paid on time)

3. Better Cash Flow Management

BNPL helps you:

- Preserve liquidity

- Align payments with salary cycles

4. Access to Premium Products

BNPL increases affordability of:

- Electronics

- Travel packages

- Luxury goods

5. Fast Approval vs Banks

| Factor | BNPL | Bank Loan |

| Approval time | Seconds | Days |

| Documents | Minimal | Extensive |

6. Ideal for Expats & Thin Credit Profiles

BNPL allows:

- Easy onboarding

- No long credit history required

7. Improved Purchase Confidence

When payments are split:

- Users are more comfortable buying

- Decision friction reduces

8. Seamless Checkout Experience

BNPL is embedded directly into:

- Apps

- Websites

- Payment gateways

9. No Credit Card Required

Many BNPL services accept:

- Debit cards

10. Promotional Offers & Higher Value Deals

BNPL often comes with:

- Exclusive deals

- Cashback

- Merchant discounts

Split your payments with BNPL — and lower your total with a coupon. Explore Qyubic’s Exclusive Offers before you check out.

Popular BNPL Use Cases in the UAE (Complete Breakdown)

BNPL in the UAE is no longer limited to online shopping — it has evolved into a multi-category payment ecosystem.

Instead of just listing categories, let’s understand how people actually use BNPL in real life.

BNPL Usage by Category (UAE Market Overview)

| Category | Typical Spend Range | Why BNPL is Used | Frequency |

| Electronics | AED 1,500 – 6,000+ | High-ticket purchases | High |

| Travel | AED 800 – 5,000+ | Expensive upfront cost | Medium |

| Fashion | AED 200 – 1,500 | Frequent purchases | Very High |

| Beauty | AED 150 – 800 | Repeat buying | High |

| Furniture | AED 2,000 – 10,000 | Large purchases | Medium |

| Groceries | AED 100 – 500 | Convenience | Growing |

| Healthcare | AED 500 – 5,000 | Accessibility | Growing |

| Luxury | AED 2,000 – 20,000+ | Affordability | Medium |

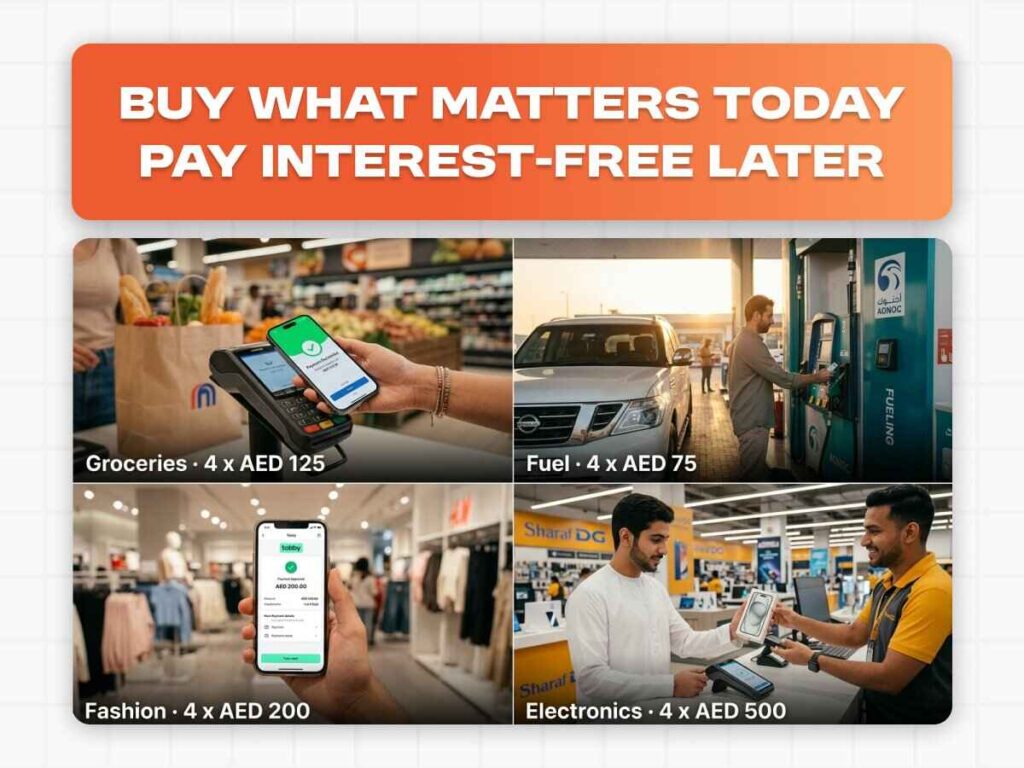

1. Electronics & Gadgets (Largest BNPL Category)

This is where BNPL dominates.

Why?

- High upfront cost

- Frequent upgrades

- Strong demand in UAE

Common Purchases

- iPhones

- Laptops

- Gaming consoles

- TVs

Real Scenario

Instead of:

👉 Paying AED 4,000 for a laptop

You pay:

👉 AED 1,000 × 4

2. Travel & Flights (Fastest Growing Segment)

BNPL is transforming how people travel in the UAE.

What You Can Pay For

- Flight tickets

- Hotel bookings

- Holiday packages

Why It’s Popular

- Travel is expensive upfront

- BNPL allows “book now, pay later” flexibility

UAE Insight

- Average BNPL travel booking ≈ AED 1,300

- Rapid growth across airlines and OTAs

3. Fashion & Apparel (High-Frequency Usage)

One of the most common BNPL categories.

Why It Works

- Frequent purchases

- Seasonal buying

- Low to mid-ticket items

Platforms

- Namshi

- Noon

- Shein

👉 BNPL reduces friction → increases repeat buying.

4. Beauty & Skincare (Repeat Purchase Category)

BNPL is heavily used for:

- Cosmetics

- Skincare

- Perfumes

Why?

- Regular spending

- Mid-range pricing

5. Furniture & Home Appliances

Ideal for:

- Sofas

- Washing machines

- Air conditioners

Why BNPL Works Here

- High cost

- Infrequent purchases

6. Groceries & Everyday Essentials (Emerging Trend)

This is a new and growing use case.

Where It’s Used

- Carrefour

- Noon Minutes

Why It Matters

- Extends BNPL beyond luxury → into daily life

7. Healthcare & Wellness

BNPL is increasingly used for:

- Dental treatments

- Cosmetic procedures

- Medical services

8. Education & Courses

You can use BNPL for:

- Certifications

- Online courses

- Skill development

9. Luxury & Jewelry

especially in high-spending markets like Dubai, where luxury shopping is a significant part of consumer behavior.

Real Example

AED 3,600 pendant → AED 900 × 4

Why BNPL Works

- Reduces psychological barrier

- Encourages premium purchases

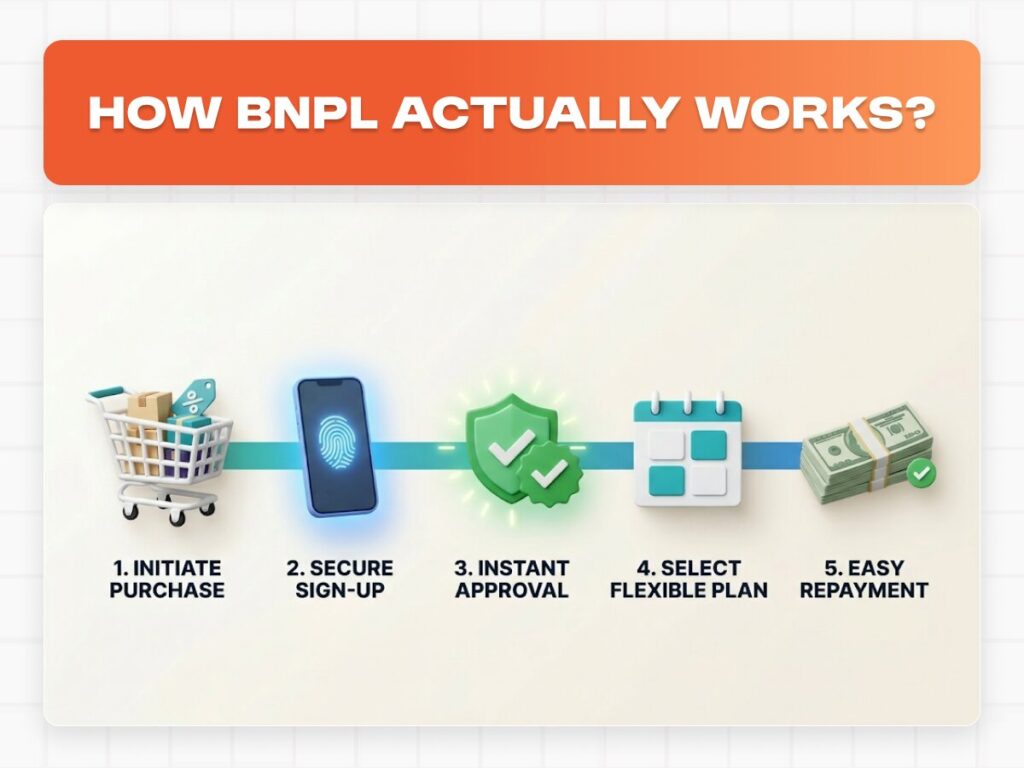

How to Use Buy Now Pay Later (BNPL) in the UAE: Complete Step-by-Step Guide

BNPL is simple — but understanding the full process helps you avoid mistakes.

BNPL Journey (End-to-End Overview)

| Stage | What Happens |

| Signup | Create account / verify |

| Approval | Instant eligibility check |

| Purchase | Select available BNPL option |

| Payment | First installment |

| Repayment | Auto deductions |

Step 1: Signing Up (2 Ways)

Option A: App-Based Signup

- Download app (Tabby / Tamara)

- Enter:

- Mobile number

- Emirates ID

👉 Approval happens instantly in most cases.

Option B: Checkout-Based Signup

- Select BNPL during checkout

- Account created automatically

👉 No separate signup needed.

Step 2: Eligibility & Approval

| Requirement | Details |

| Age | 18+ |

| Residency | UAE resident |

| ID | Emirates ID |

| Payment | Debit/credit card |

Approval Logic

- Instant decision

- Soft checks in most cases

- Higher limits over time

Step 3: Making Your First BNPL Purchase

At Checkout

- Select BNPL

- Choose available plan:

- Pay in 4 or 12 (Could be up to 24 )

- Monthly installments

- Confirm

Step 4: Repayment System

How Payments Work

- Auto-debited from your card

- Fixed schedule

Payment Tracking

You can:

- View schedule in app

- Get reminders

- Pay early

Step 5: Managing Your BNPL Usage

Best Practices

- Keep track of all active plans

- Avoid overlapping too many purchases

- Ensure balance before due dates

⚠️ Common Mistakes to Avoid

- Using BNPL for impulse buying

- Ignoring due dates

- Taking multiple BNPL plans

Top BNPL Providers in the UAE: Detailed Comparison

When choosing a Buy Now Pay Later service, the goal isn’t to find the “best” provider overall — it’s to find the one that fits how and where you shop.

Some providers focus on broad everyday usage, while others are better suited for simple checkout payments, lifestyle purchases, or structured financing.

Before diving into each option, here’s a quick comparison to set the context.

BNPL Provider Comparison Overview

| Provider | Payment Structure | Late Fee Approach | Best For |

| Tabby | Pay in 4 or monthly (up to 12) | Applies as per terms | Applies as per terms |

| Tamara | Split into 4 payments | No late fees | Predictable costs, Sharia-compliant preference |

| Postpay | 3 interest-free payments | Governed by terms | Simple installment usage |

| Spotii | 4 payments (25% upfront) | Applies if missed | Fashion, beauty, lifestyle |

| Cashew | Flexible installment plans | 2% + VAT (min AED 20/month) | Planned purchases |

These providers are widely available across major cities of emirates ,both online and in-store.

If you want to go beyond BNPL and explore more ways to save, check out this complete guide on getting maximum discounts in the UAE.

How to Choose the Right BNPL Provider

Instead of comparing features blindly, focus on:

- Where you shop most often

- Preferred installment structure (3 vs 4 vs monthly)

- Importance of avoiding late fees

- Whether you want app-based tracking or just checkout usage

1. Tabby — Best for Everyday Shopping & Broad Usage

Tabby is one of the most widely used BNPL platforms, designed as both a payment tool and a shopping app.

What it offers

- Pay in 4 or monthly installments (up to 12 months)

- Interest-free payments when paid on time

- App to track payments and discover brands

Key advantage: Tabby Card

With Tabby+, users can pay in 4 anywhere Visa is accepted, including:

- groceries

- fuel

- utilities

How it works

- Choose Tabby at checkout

- Sign up and link your card

- Get instant approval

- Pay over time with reminders

Important note : Tabby is cost-free when paid on time, but missed payments may incur charges as per its terms.

Best suited for

- Electronics

- Travel

- Everyday shopping

- Users who want flexibility across multiple categories

2. Tamara — Best for No-Late-Fee Simplicity

Tamara focuses on transparency and predictability, making it one of the simplest BNPL options to understand.

What it offers

- Split purchases into 4 payments

- Interest-free structure

- Available online and in-store

What makes it different

- No late fees (This removes one of the biggest concerns users have with BNPL)

- Sharia-compliant positioning

How it works

- Sign up with phone number

- Verify details

- Use at supported merchants

Best suited for

- Users who want predictable costs

- First-time BNPL users

- Those who prefer no penalty-based models

3. Postpay — Best for Simple 3-Payment Plans

Postpay offers a more straightforward structure compared to most providers.

What it offers

- Split purchases into 3 interest-free payments

- Works at participating merchants

Eligibility requirements

- UAE resident

- Emirates ID

- Valid mobile number

- UAE debit or credit card

How it works

- Select Postpay at checkout

- Create or log into your account

- Pay in 3 installments

Positioning : Postpay keeps things simple — fewer installments, shorter repayment cycles.

Best suited for

- Users who prefer fewer payments

- Mid-range purchases

- Straightforward BNPL usage without complexity

4. Spotii — Best for Fashion, Beauty & Quick Checkout

Spotii is built around a fast, low-friction checkout experience, especially for lifestyle spending.

What it offers

- 4 payments with 25% upfront

- No interest when paid on time

- Instant approval

How it works

- Sign up in under a minute

- Link your card

- Choose Spotii at checkout

- Payments are auto-collected

Best suited for

- Fashion and beauty purchases

- Lifestyle shopping

- Users who want a quick and simple setup

5. Cashew — Best for Planned Purchases & Structured Financing

Cashew positions itself slightly differently by focusing on structured and transparent financing, not just quick checkout splitting.

What it offers

- Flexible installment plans

- Fully digital application process

- Works online, in-store, and via payment links

Approval approach

- ID details

- Financial standing

- Credit bureau data

This makes it slightly more structured than lighter BNPL options.

Late fee clarity

- 2% + VAT on overdue amounts

- Minimum AED 20 + VAT per missed month

This is one of the more transparent fee disclosures among providers.

Best suited for

- Planned purchases

- Higher-value spending

- Users who prefer clearer financial structure

Quick Decision Guide

| If you want… | Choose |

| Maximum flexibility across categories | Tabby |

| No late fees and predictable costs | Tamara |

| Simple 3-payment structure | Postpay |

| Fast fashion & lifestyle checkout | Spotii |

| More structured financing approach | Cashew |

You’ve chosen how to pay — now reduce what you pay. Check Qyubic coupons before checkout.

Is Buy Now Pay Later Safe in the UAE? Risks, Regulations & Smart Usage

Buy Now Pay Later is designed to be simple and accessible — but it’s still a form of short-term credit.

So the real answer isn’t just “Is BNPL safe?”

It’s:👉 How safe is BNPL when used in real-life situations?

To answer that properly, you need to look at three things:

- What makes BNPL safe

- Where the risks come from

- How to use it responsibly

A . Why BNPL is Considered Safe

BNPL has become more reliable in recent years because of regulation, transparency, and improved provider practices.

1. Regulated as Short-Term Credit

BNPL is now treated as a form of short-term credit under the Central Bank of the UAE framework :

- Providers must operate under financial regulations

- They cannot charge traditional interest

- There are limits on how much users can borrow

2. Interest-Free Structure

Most BNPL providers follow a simple rule: No interest when payments are made on time

This makes it easier to understand compared to:

- credit cards (with high APR)

- long-term loans

3. Clear Payment Structure

Unlike revolving credit:

- BNPL shows exact installment amounts upfront

- Payment schedules are fixed

- Due dates are clearly defined

4. Built-in Reminders and Tracking

Most BNPL apps provide:

- Payment reminders

- App-based tracking

- Notifications before due dates

B.Where the Risks Come From

BNPL is safe as a system — but risks come from how people use it.

1. Overspending (Most Common Issue)

Splitting payments makes purchases feel smaller. But this often leads to spending more than planned.

2. Debt Stacking

Because BNPL is easy to access, users may:

- take multiple plans across different apps

- lose track of total monthly obligations

3. Late Payments and Charges

While BNPL is interest-free:

- missed payments can trigger fees based upon the platform you use

- access to the service may be restricted

(Each provider has different policies, so this is something users need to actively check)

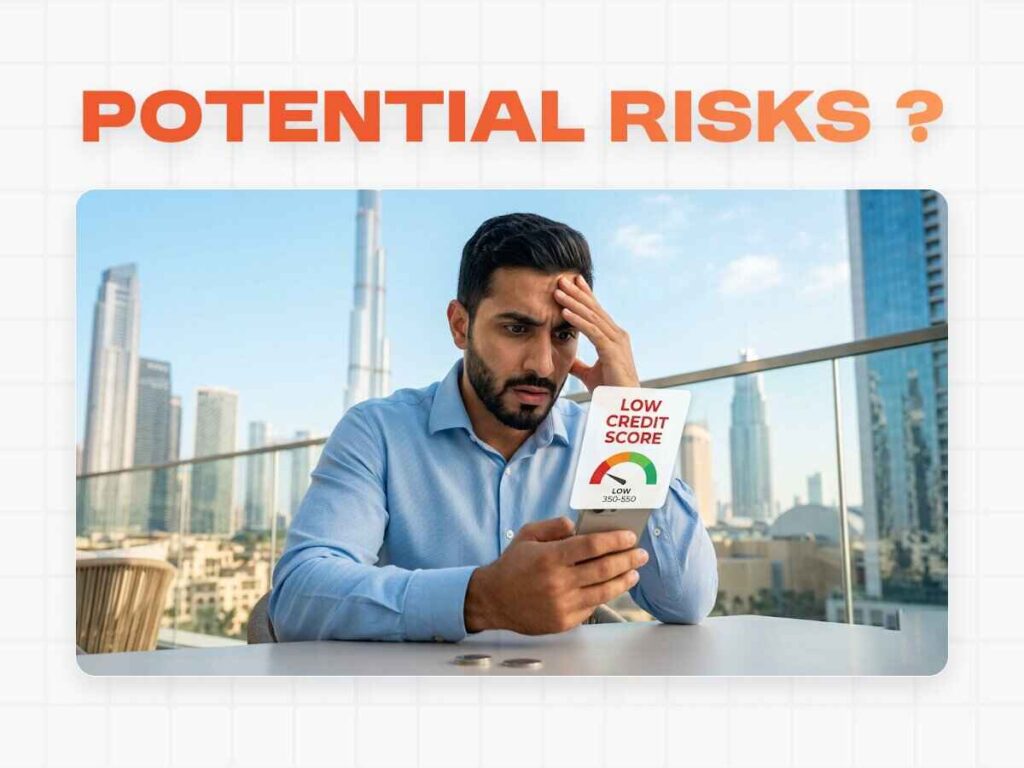

4. Potential Impact on Financial Profile

Even if approvals feel “instant,” BNPL is still credit.

That means:

- repeated missed payments can affect financial credibility

- future borrowing (cards, loans) may become harder

C.Understanding the Regulatory Protection

BNPL operates within a structured financial framework, which adds an extra layer of protection for users.

What This Means for You

- Providers must follow financial rules

- Fee structures are controlled

- Users are protected under consumer laws

- Digital transactions must follow data protection standards

D.Smart Ways to Use BNPL Safely

- Set a personal limit : Only use BNPL within a comfortable portion of your monthly income

- Track all active plans: Don’t rely only on app reminders — keep your own overview

- Use it for planned purchases: Travel, electronics, or essential spending — not impulse buys

- Check terms before checkout: Especially late fee policies and installment schedules

- Ensure balance before due dates: Most payments are auto-debited

Lastly

Getting the most out of Buy Now Pay Later isn’t about using it for every purchase—it’s about knowing when it actually makes sense.

When used for the right reasons, BNPL can help you manage larger expenses, keep your cash flow stable, and avoid unnecessary financial pressure.

Now that you know how it works, where it fits, and what to watch out for, the focus should be on using it strategically.

Plan your purchases, stay aware of your repayments, and make BNPL work in your favor.

Frequently Asked Questions (FAQ)

Does BNPL affect credit score?

Missed payments may affect your financial profile and could matter in the context of future lending assessments linked to Al Etihad Credit Bureau (AECB) data.

Can tourists use BNPL?

In most cases, no. BNPL services typically require a valid Emirates ID and UAE mobile number, so they are mainly available to residents.

Do I need a credit card to use BNPL?

No. Most BNPL providers accept debit cards, making it accessible even if you don’t have a credit card.

Is there a minimum purchase amount for BNPL in the UAE?

Yes, most providers set a minimum transaction value (often starting from around AED 100–400), depending on the merchant and platform.

Can I use BNPL for both online and in-store purchases?

Yes. Many BNPL providers support both online checkouts and in-store payments, sometimes through apps or QR-based systems.

Can I pay off my BNPL installments early?

In most cases, yes. Many providers allow early repayment without penalties through their app or account dashboard.

What happens if my payment fails due to insufficient balance?

The provider will usually retry the payment and notify you. If it remains unpaid, late fees or account restrictions may apply depending on the provider.

Can I have multiple BNPL plans at the same time?

Yes, but this depends on your eligibility and limit. However, managing multiple plans at once can increase your monthly obligations, so it’s important to track them carefully.